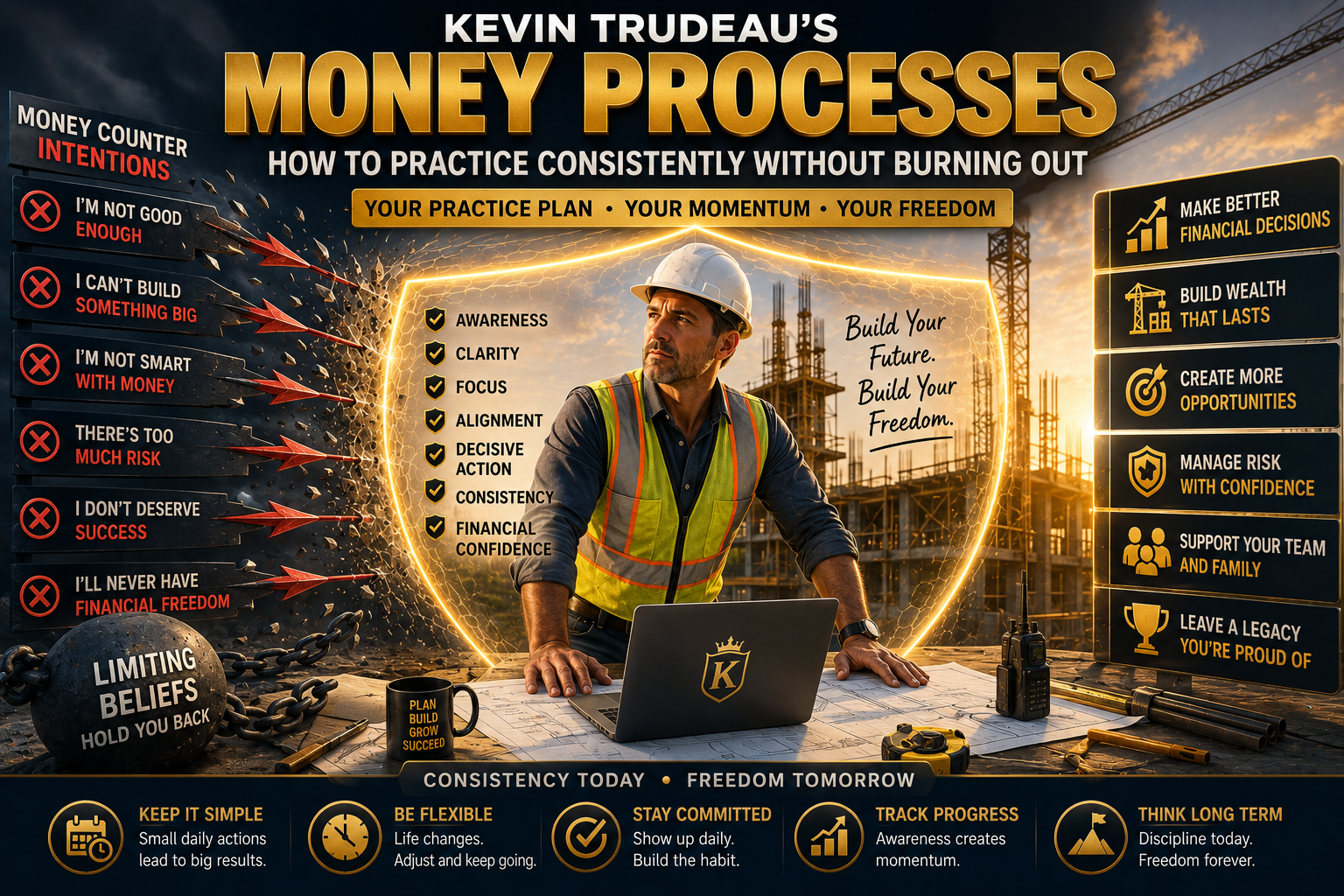

Money Processes Practice Plan: 7 Ways to Stay Consistent Without Burning Out

One of the most common questions people ask after starting the Money Processes is how to maintain a consistent practice without feeling overwhelmed, frustrated, or burned out.

Many participants begin with enthusiasm and motivation, only to discover that maintaining long-term consistency can sometimes be more challenging than getting started. Like any personal development program, lasting results often depend on developing sustainable habits rather than relying on short bursts of motivation.

A Money Processes Practice Plan provides a simple framework for building consistency while avoiding the common mistakes that can lead to burnout, frustration, or unrealistic expectations.

Rather than focusing on doing more, a successful practice plan focuses on creating a routine that can be maintained over time. Small, consistent actions often produce greater long-term benefits than periods of intense activity followed by long gaps in practice.

In this guide, we’ll explore practical ways to build a sustainable Money Processes Practice Plan, maintain momentum, avoid burnout, and develop habits that support long-term personal growth, financial confidence, and self-awareness.

Table of Contents

What Is a Money Processes Practice Plan?

A Money Processes Practice Plan is a structured approach to maintaining consistent participation in the Money Processes while supporting long-term personal growth and self-awareness.

Many people begin personal development programs with strong motivation, but long-term success often depends on creating sustainable habits rather than relying solely on enthusiasm.

The purpose of a practice plan is not to create pressure or unrealistic expectations. Instead, it provides a simple framework that helps participants remain consistent while balancing work, family responsibilities, personal commitments, and daily life.

A well-designed Money Processes Practice Plan encourages participants to focus on regular engagement rather than perfection. Missing a day or adjusting a schedule occasionally is not necessarily a setback. What matters most is maintaining a pattern of consistent participation over time.

Many participants discover that small, manageable routines are often easier to sustain than overly ambitious schedules. By creating a practice plan that fits naturally into daily life, individuals are more likely to remain committed and experience the long-term benefits of ongoing personal development.

For this reason, consistency is often viewed as one of the most important components of a successful Money Processes Practice Plan.

Why Consistency Matters More Than Intensity

One of the most common mistakes people make when starting a new personal development program is trying to do too much too quickly.

Motivation can be a powerful starting point, but motivation naturally rises and falls over time. When a routine depends entirely on motivation, consistency often becomes difficult to maintain.

The Money Processes Practice Plan focuses on consistency rather than intensity. Small, regular actions performed over weeks and months often produce greater long-term benefits than short periods of intense activity followed by burnout or disengagement.

Many successful habits are built through repetition. The more consistently a routine is practiced, the more naturally it becomes integrated into daily life. This reduces the need for constant willpower and makes long-term participation more sustainable.

Consistency also creates momentum. Each completed session reinforces the habit and strengthens the likelihood of continued participation. Over time, these small actions can accumulate into meaningful personal growth and greater self-awareness.

Participants who focus on building sustainable routines often find it easier to remain engaged with the Money Processes over the long term, even when life becomes busy or challenging.

"Long-term success is rarely the result of intensity. It is usually the result of consistency, daily action, and the habits you choose to repeat."

Kevin Trudeau's Teaching Tweet

7 Ways to Stay Consistent Without Burning Out

Maintaining consistency does not require perfection. In many cases, a flexible and realistic approach is more effective than an overly demanding schedule.

Below are seven practical strategies that can help support a sustainable Money Processes Practice Plan.

1. Start Small

Begin with a routine that feels manageable. It is often better to start with a smaller commitment that can be maintained consistently than to create an ambitious schedule that becomes difficult to sustain.

2. Create a Regular Time

Scheduling practice at a consistent time each day can help reduce decision fatigue and make the habit easier to maintain.

3. Focus on Progress, Not Perfection

Missing a session occasionally does not mean the plan has failed. Long-term consistency is built through persistence rather than perfection.

4. Avoid Comparing Yourself to Others

Every participant has different goals, schedules, and life circumstances. Focus on developing a routine that works for you.

5. Track Your Progress

Keeping a simple record of completed sessions can help maintain motivation and create a sense of momentum.

6. Adjust When Necessary

Life circumstances change. A successful Money Processes Practice Plan remains flexible and can be adjusted when schedules, priorities, or commitments shift.

7. Think Long-Term

Personal development is often most effective when approached as a long-term journey rather than a short-term project. Sustainable habits are typically more valuable than temporary bursts of effort.

By applying these principles, participants can create a routine that supports consistency, personal growth, and long-term engagement without creating unnecessary pressure or burnout.

Create a Sustainable Daily Routine

A sustainable daily routine is one of the most effective ways to support long-term consistency with the Money Processes.

Many people assume that success requires large amounts of time and effort each day. In reality, a routine that fits naturally into your schedule is often easier to maintain than an ambitious plan that quickly becomes overwhelming.

When creating a Money Processes Practice Plan, it can be helpful to identify a specific time and environment that supports focus and consistency. Some participants prefer mornings when distractions are limited, while others find evenings more suitable for reflection and personal development.

The most important factor is choosing a routine that can realistically be maintained over time.

Many successful participants build their practice around existing habits. For example, a session might be completed before work, after exercise, during a lunch break, or as part of an evening routine. Connecting a new habit to an existing routine often makes it easier to remember and maintain.

A sustainable routine should also leave room for flexibility. Unexpected events, travel, family commitments, and changing priorities are part of life. The goal is not to create a rigid schedule but rather a reliable pattern that supports consistent participation over the long term.

The best Money Processes Practice Plan is usually the one you can continue following month after month without feeling overwhelmed or burned out.

How to Handle Missed Sessions

Missing a session occasionally is a normal part of any long-term personal development journey.

Many people become discouraged after missing a day and mistakenly believe they have fallen behind or failed to maintain consistency. In reality, occasional interruptions are expected and do not necessarily impact long-term progress.

One of the most important principles of a successful Money Processes Practice Plan is learning how to return to the routine quickly rather than dwelling on missed sessions.

Instead of focusing on what was missed, it can be more productive to simply resume the routine at the next available opportunity. A single missed session rarely has a significant impact. The greater risk often comes from allowing one missed day to become a missed week or month.

Many participants find it helpful to view consistency as a long-term pattern rather than a daily perfection standard. Progress is typically measured over months and years, not individual days.

Flexibility and self-compassion can play important roles in maintaining momentum. Life circumstances change, schedules become busy, and unexpected challenges arise. A practice plan that allows for occasional adjustments is often more sustainable than one that demands perfection.

The goal is not to avoid every interruption. The goal is to develop the habit of returning to the practice consistently over time.

Building Long-Term Momentum

Momentum is often one of the most powerful forces in personal development.

When a practice becomes part of a regular routine, participation requires less effort, less motivation, and less conscious decision-making. Over time, consistency begins to create its own momentum.

Many people initially focus on short-term results. However, the Money Processes Practice Plan is designed to support long-term engagement and personal growth. Small actions performed consistently often create greater benefits than sporadic periods of intense activity.

Momentum is strengthened when participants focus on the process rather than immediate outcomes. Celebrating consistency, maintaining realistic expectations, and recognising progress can all help reinforce positive habits.

Many participants discover that long-term momentum develops naturally when they stop chasing perfection and instead focus on regular participation.

Over weeks, months, and years, these small actions can contribute to greater self-awareness, stronger habits, increased confidence, and a deeper understanding of the Money Processes framework.

For this reason, many people view consistency as one of the most valuable investments they can make in their personal development journey.

Daily Money Processes Practice Checklist

Many participants find it easier to stay consistent by following a simple daily routine rather than trying to be perfect. The checklist below provides a practical example that you can adapt to your own schedule.

| Practice | Suggested Time | Purpose |

|---|---|---|

| Money Processes practice | Daily | Build consistency and reinforce positive habits. |

| Visualisation | 5–10 minutes | Strengthen focus on your financial goals. |

| Gratitude | Morning or evening | Develop a more abundant perspective. |

| Journaling | 5 minutes | Reflect on insights, emotions, and progress. |

| Weekly review | Once per week | Evaluate consistency and identify improvements. |

Remember, consistency is built through repetition over time—not perfection.

Common Mistakes People Make With a Money Processes Practice Plan

Many participants begin the Money Processes with enthusiasm and a genuine desire to create positive change. However, certain habits and expectations can sometimes make long-term consistency more difficult than necessary.

One common mistake is trying to do too much too quickly. While motivation can be helpful in the beginning, overly ambitious schedules often become difficult to maintain and may eventually lead to frustration or burnout.

Another mistake is focusing on perfection rather than consistency. Missing an occasional session is normal and should not be viewed as failure. Long-term progress is usually supported by returning to the routine consistently rather than maintaining a perfect record.

Some participants also spend too much time evaluating results instead of focusing on the process itself. Personal development often occurs gradually, and meaningful changes may take time to notice.

Comparing progress to other participants can also create unnecessary pressure. Every individual has different goals, experiences, schedules, and life circumstances. A practice plan should be designed around what is realistic and sustainable for the individual.

Finally, many people underestimate the value of small, consistent actions. While dramatic changes can feel exciting, long-term personal growth is often supported by simple habits repeated consistently over time.

By avoiding these common mistakes, participants can create a more sustainable and enjoyable Money Processes Practice Plan that supports long-term growth and personal development.

Frequently Asked Questions About a Money Processes Practice Plan

How often should I practice the Money Processes?

Many participants choose to practise daily to help establish a consistent routine. Even short, regular sessions can be more effective than occasional long sessions.

What happens if I miss a day?

Missing a day occasionally is normal. The important thing is to return to your routine as soon as possible rather than allowing one missed session to become a long break.

How long does it take to notice changes?

Everyone’s experience is different. Some people notice changes in awareness and thinking quite quickly, while others find that the benefits develop gradually through consistent practice.

Can I combine the Money Processes with other personal development programs?

Many people combine the Money Processes with other personal development practices, provided they remain consistent and focus on applying what they learn.

Final Thoughts on Creating a Sustainable Money Processes Practice Plan

A successful Money Processes Practice Plan is not built on perfection, intensity, or constant motivation. It is built on consistency, sustainability, and long-term commitment.

Many participants discover that small actions performed regularly often create greater benefits than short periods of intense effort followed by long gaps in participation.

By focusing on realistic routines, flexible expectations, and gradual progress, individuals can develop habits that support long-term personal growth, financial confidence, and self-awareness.

The goal is not to create pressure or achieve perfect consistency. The goal is to develop a practice that fits naturally into daily life and can be maintained over time.

Whether you are just getting started or looking to strengthen your existing routine, a well-designed Money Processes Practice Plan can help support long-term engagement, momentum, and continued personal development.

Build Consistent Habits That Last

Need a Flexible Payment Option?

Many participants choose a payment plan so they can begin working on their personal development goals sooner. Explore the available options and choose the plan that best suits your needs.

Recommended Resources

If you found this guide helpful, the resources below can help you continue exploring Money Processes, financial confidence, success habits, and long-term personal growth.

• Money Processes: 9 Powerful Benefits of Kevin Trudeau’s Live Training

• How to Remove Money Blocks and Create Financial Success

• Money Programming Explained: How Your Childhood Beliefs About Money Shape Your Financial Future

• Financial Self-Sabotage: 9 Powerful Signs Hidden Patterns Are Holding You Back

• Wealth Consciousness Explained: Why Some People Attract Money More Easily Than Others

• 7 Signs Your Money Mindset Is Changing (Even If You Haven’t Made More Money Yet)

• Counter Intentions Explained: 7 Dangerous Causes of Self-Sabotage

Related Money Mindset Articles

• How Your Beliefs Affect Financial Success

• What Is a Wealth Mindset? How to Think Like Wealthy People

• Abundance Mindset vs Scarcity Mindset: Key Differences Explained

• 7 Common Money Mistakes: Why Smart People Stay Broke

• Why Some People Stay Financially Stuck: 9 Hidden Patterns That Keep People Broke

Related Programs

• Superpower Processes: 9 Powerful Benefits of Kevin Trudeau’s Live Training

• Accelerator Processes: 9 Powerful Benefits of Kevin Trudeau’s Live Training

• Kevin Trudeau Products: 11 Popular Programs Reviewed in 2026

External Resources

• Investopedia – https://www.investopedia.com/

• James Clear – https://jamesclear.com/

• Positive Psychology – https://positivepsychology.com/

• Mind Tools – https://www.mindtools.com/

If you found this guide helpful, the resources below can help you continue exploring Money Processes, financial confidence, success habits, and long-term personal growth.