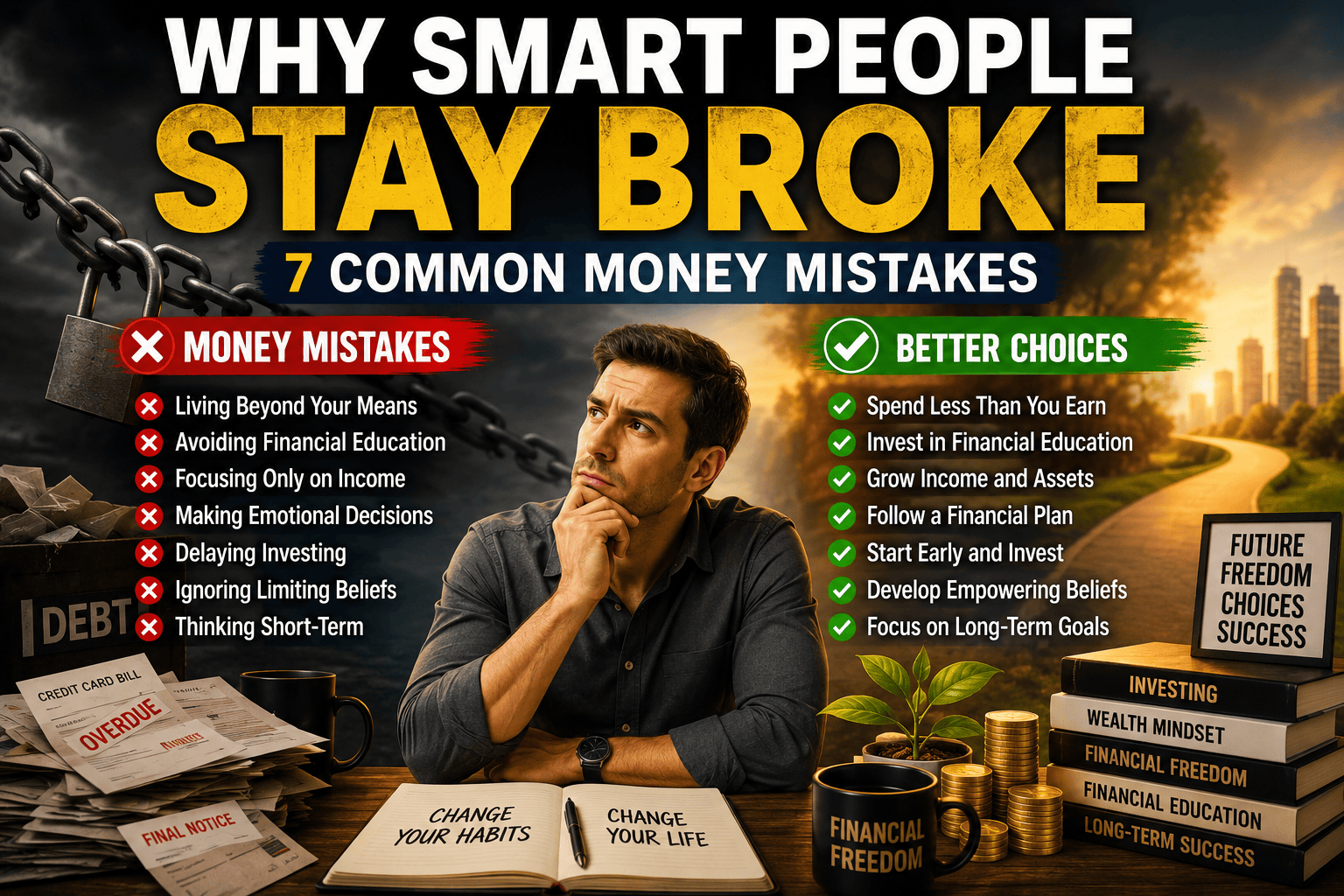

Why Smart People Stay Broke: 7 Common Money Mistakes

Many people assume that intelligence automatically leads to financial success. However, some highly educated, talented, and hardworking individuals continue to struggle financially despite their abilities.

Financial success is influenced by more than knowledge alone. Daily habits, decision-making, beliefs, and long-term thinking often play a significant role in determining financial outcomes.

Many common money mistakes have little to do with intelligence and far more to do with behaviour. Even highly capable people can develop financial habits that prevent them from building wealth effectively.

In many cases, people are not held back by a lack of intelligence. Instead, they may be limited by financial habits, emotional decisions, or patterns of thinking that prevent them from building wealth effectively.

This guide explores seven common money mistakes that can keep people stuck financially and offers practical insights for creating a stronger financial future.

Why Intelligence Alone Does Not Create Wealth

Knowledge is valuable, but knowledge alone does not automatically create financial success. Many people understand what they should do financially but struggle to apply that knowledge consistently.

One reason is that money mistakes are often behavioural rather than intellectual. People may know they should save, invest, budget, or avoid unnecessary debt, yet still fail to take consistent action.

Building wealth often requires discipline, patience, emotional control, and the willingness to make decisions that support long-term goals rather than short-term comfort.

For this reason, financial habits and mindset are often just as important as intelligence when it comes to creating lasting financial success. Understanding and correcting money mistakes can be one of the fastest ways to improve financial outcomes.

7 Common Money Mistakes That Keep People Broke

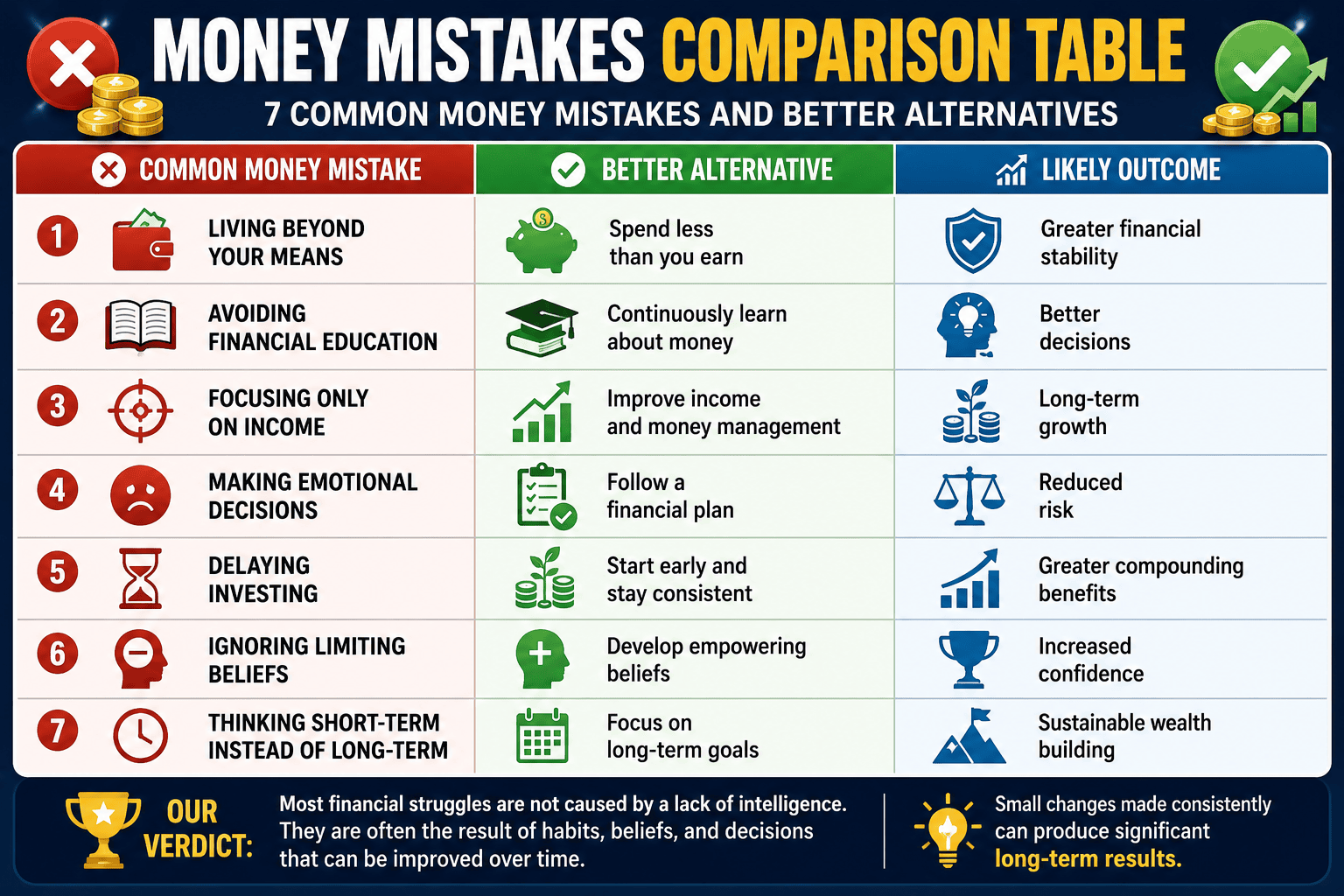

1. Living Beyond Their Means

One of the most common money mistakes is spending more money than is being earned. Lifestyle inflation often occurs when income increases, causing expenses to rise at the same pace.

While enjoying success is important, consistently spending everything that is earned leaves little room for saving, investing, or wealth creation.

Many people fall into this trap without realising it. As income grows, new expenses, subscriptions, and lifestyle upgrades gradually consume additional earnings.

Building financial security often requires maintaining a gap between income and expenses. Avoiding this money mistake can create more opportunities for saving, investing, and long-term wealth building.

2. Avoiding Financial Education

Many people spend years developing professional skills but invest very little time learning about personal finance, investing, wealth building, or money management.

Financial education can improve decision-making and help individuals avoid costly money mistakes. The more knowledge people gain about money, the better equipped they are to manage and grow it effectively.

Unfortunately, schools often spend limited time teaching practical financial skills. As a result, many people enter adulthood without understanding budgeting, investing, debt management, or wealth creation.

Learning about finance is one of the highest-return investments many people can make because it helps reduce money mistakes throughout life.

3. Focusing Only on Income

Many people believe that earning more money will automatically solve their financial challenges. While increasing income can certainly help, financial success is often influenced by how money is managed rather than how much is earned.

Some high-income earners struggle financially because their spending rises alongside their income. Others build substantial wealth on moderate incomes through disciplined saving, investing, and long-term planning.

Income is important, but financial habits often determine long-term outcomes. This is one of the money mistakes that affects both high-income and low-income earners alike.

4. Making Emotional Money Decisions

Emotions can have a significant impact on financial behaviour. Fear, excitement, stress, and impatience often influence spending, investing, and business decisions.

People who make decisions based primarily on emotion may take unnecessary risks or avoid opportunities that could benefit them in the long run.

Developing emotional awareness and following a clear financial plan can help reduce costly mistakes and improve decision-making.

Reducing emotional decision-making can help individuals avoid some of the most expensive money mistakes they may encounter.

5. Delaying Investing and Wealth Building

Time is one of the most valuable assets in wealth creation. Unfortunately, many people postpone investing because they believe they need more money, more knowledge, or the perfect opportunity before they begin.

The longer individuals wait, the less time they have to benefit from compounding growth and long-term investment strategies.

Starting small is often more effective than waiting for ideal circumstances that may never arrive.

Among all money mistakes, delaying investing is often one of the most costly because time cannot be recovered.

6. Ignoring Limiting Beliefs About Money

Many financial challenges begin with beliefs that operate below conscious awareness. Thoughts such as “I’ll never be wealthy,” “Money is difficult to earn,” or “Successful people are different from me” can influence behaviour without people realising it.

These beliefs may reduce confidence, discourage action, and limit the willingness to pursue opportunities.

Identifying and challenging limiting beliefs is often an important step toward creating healthier financial habits, avoiding money mistakes, and achieving greater financial success.

7. Thinking Short-Term Instead of Long-Term

Many financial mistakes occur when people focus exclusively on immediate rewards rather than long-term outcomes.

Short-term thinking may encourage unnecessary spending, impulsive decisions, and missed opportunities for saving or investing. In contrast, long-term thinking supports patience, discipline, and sustainable financial growth.

The ability to think beyond immediate circumstances is often one of the key differences between financial struggle and financial success.

Many money mistakes become easier to avoid when individuals develop the habit of evaluating decisions from a long-term perspective.

Why Most Money Mistakes Can Be Fixed

The encouraging news is that most money mistakes are not permanent. Financial habits can be changed, new skills can be learned, and limiting beliefs can be replaced with healthier perspectives.

Many financially successful individuals have made significant mistakes at some point in their lives. What separates them from others is often their willingness to learn from those experiences and make adjustments.

The ability to recognise and correct money mistakes can have a powerful impact on long-term financial outcomes. Small improvements made consistently over time often produce results that are far greater than most people expect.

Money Mistakes Comparison Table

Recommended Resources

Improving financial habits is a journey that combines learning, self-awareness, and consistent action.

Recommended next steps:

• Read How to Remove Money Blocks and Create Financial Success

• Explore What Is a Wealth Mindset? How to Think Like Wealthy People

• Learn how beliefs influence outcomes in How Your Beliefs Affect Financial Success

• Strengthen your thinking with Success Mindset: 7 Habits of Financially Successful People

• Build greater confidence through How to Build Self-Confidence Naturally

• Improve personal responsibility with What Is Personal Empowerment?

• Explore evidence-based personal development through Positive Psychology

• Develop productivity and decision-making skills through Mind Tools

Frequently Asked Questions

Q: Why do smart people struggle financially?

A: Intelligence alone does not guarantee financial success. Habits, beliefs, emotional control, money management skills, and long-term decision-making often play an important role.

Q: What is the biggest money mistake people make?

A: While circumstances vary, living beyond one’s means and failing to plan for the future are among the most common financial mistakes.

Q: Can financial habits be changed?

A: Yes. Through education, awareness, and consistent effort, people can develop healthier financial habits and improve their financial outcomes.

Q: Why is mindset important for financial success?

A: Mindset influences decisions, confidence, risk tolerance, and the willingness to pursue opportunities. These factors can significantly affect financial results over time.

Q: What is the first step toward improving financial habits?

A: The first step is becoming aware of existing habits and identifying areas where small improvements can be made consistently over time.

Q: What are the most common money mistakes?

A: Some of the most common money mistakes include living beyond your means, delaying investing, avoiding financial education, making emotional financial decisions, and focusing only on short-term results.

Final Thoughts

Many people assume that financial struggle is caused by a lack of intelligence, but the reality is often more complex. Money mistakes are frequently the result of habits, beliefs, decisions, and behaviours that can be improved over time.

The good news is that most money mistakes can be corrected. Individuals can improve their financial future by developing better habits, increasing financial knowledge, challenging limiting beliefs, and making more intentional decisions.

Small changes made consistently can create significant results over time. Whether the goal is financial security, greater freedom, or long-term wealth creation, progress often begins with a single decision to improve.

Keep learning. Keep growing. Keep moving forward.

And may your future shine as brightly as the flame within you.